A classified balance sheet is a fundamental financial statement used by businesses to present their financial position at a specific point in time. It offers a clear and organized breakdown of a company’s assets, liabilities, and equity, categorized into specific groups to give stakeholders a more detailed understanding of its financial health. Unlike a simple balance sheet, which lists all accounts without any grouping, a classified balance sheet helps distinguish between different types of financial items, making it easier to interpret and analyze financial data.

Understanding the Structure of a Classified Balance Sheet

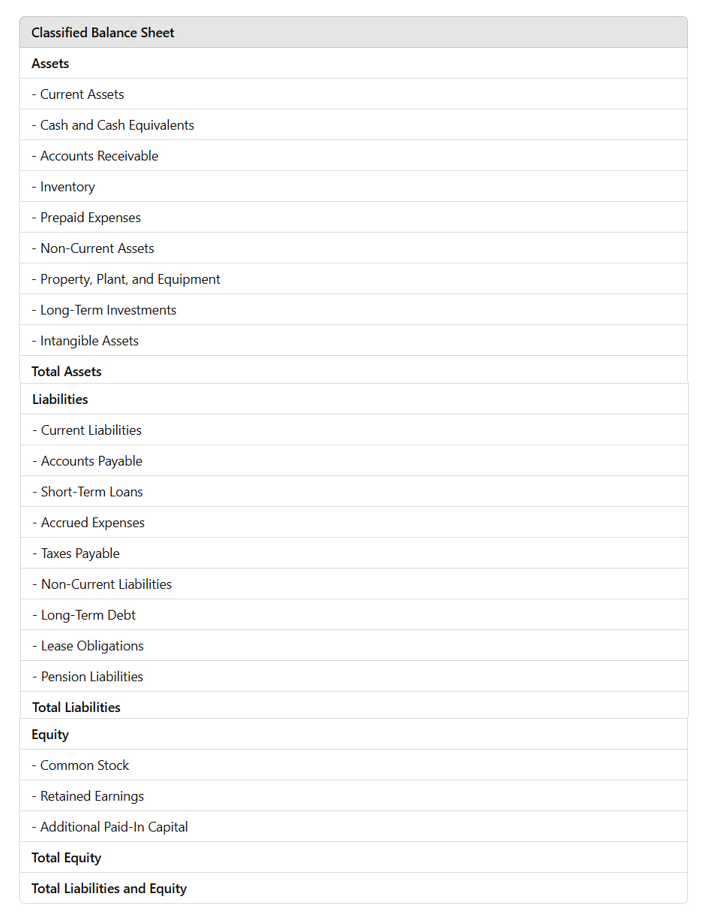

A classified balance sheet categorizes a company’s financial elements into three primary sections:

- Assets – These represent what a company owns. Assets are items of value that the business has control over and can utilize to generate future economic benefits. They are further divided into:

- Current Assets: These are short-term resources that are expected to be converted into cash or used up within one year. Common examples include:

- Cash and Cash Equivalents: Liquid assets such as petty cash, bank deposits, and marketable securities.

- Accounts Receivable: Money owed to the business by customers for products or services already provided.

- Inventory: Goods that a company holds for resale or raw materials to be used in production.

- Short-Term Investments: Investments that are meant to be held for a short period, often up to one year.

- Prepaid Expenses: Payments made in advance for goods or services that are yet to be received.

- Non-Current Assets: These are long-term resources that the company plans to hold and use for more than one year. Examples include:

- Property, Plant, and Equipment (PP&E): These are tangible assets like buildings, machinery, and vehicles that are used in the operations of the business.

- Long-Term Investments: Investments that are intended to be held for more than one year, such as stock in other companies or bonds.

- Intangible Assets: These include patents, trademarks, copyrights, and goodwill, which cannot be touched but hold value.

- Current Assets: These are short-term resources that are expected to be converted into cash or used up within one year. Common examples include:

- Liabilities – These represent what a company owes to others. Liabilities are obligations that the business must settle over a specific period. Similar to assets, liabilities are also divided into:

- Current Liabilities: These are short-term obligations that need to be paid within one year. Examples include:

- Accounts Payable: Money the company owes to suppliers or vendors for goods or services already received.

- Short-Term Loans: Loans that the company is expected to repay within the next 12 months.

- Accrued Expenses: Expenses that the business has incurred but not yet paid, such as wages payable or utility bills.

- Taxes Payable: Tax obligations due to the government within the current fiscal year.

- Non-Current Liabilities: These are long-term obligations that the company will pay after more than one year. Examples include:

- Long-Term Debt: Loans and other financial obligations that the business plans to repay over an extended period, typically more than a year.

- Lease Obligations: Long-term rental agreements where payments will extend beyond one year.

- Pension Liabilities: The company’s responsibility to pay retirement benefits to its employees in the future.

- Current Liabilities: These are short-term obligations that need to be paid within one year. Examples include:

- Equity – This represents the owner’s residual interest in the assets of the company after all liabilities have been deducted. It reflects the ownership interest in the business, including retained earnings and contributions from shareholders. The main components of equity include:

- Common Stock: The total amount of shares issued by the company to investors.

- Retained Earnings: The cumulative profits or losses that the company has accumulated over time, which are reinvested in the business rather than distributed as dividends.

- Additional Paid-In Capital: The money invested into the company by shareholders that exceeds the par value of shares.

The Importance of a Classified Balance Sheet

The classified balance sheet serves multiple purposes and provides critical information to various stakeholders, including investors, creditors, management, and regulatory bodies. Its key importance lies in:

- Improved Financial Analysis: By categorizing assets and liabilities, the classified balance sheet helps stakeholders analyze a company’s financial health and liquidity. It allows them to distinguish between short-term obligations and long-term investments, helping to gauge the company’s ability to pay its debts in the near future.

- Liquidity Assessment: Liquidity is a crucial aspect of financial health. The classified balance sheet clearly separates current assets from non-current ones, offering insight into a company’s short-term financial stability. Companies with a higher proportion of current assets compared to liabilities are generally more liquid and capable of meeting short-term obligations.

- Solvency Evaluation: Solvency refers to the company’s ability to meet its long-term obligations. The classified balance sheet categorization of long-term liabilities helps in evaluating solvency. Companies with a higher proportion of long-term assets compared to long-term liabilities show strong solvency.

- Financial Planning: For management, a classified balance sheet provides a framework for financial planning. It highlights areas where the company might need to improve efficiency or increase liquidity to ensure long-term sustainability.

- Risk Assessment: Lenders and investors often analyze the classified balance sheet to assess a company’s financial risk. They look at the proportion of debt relative to equity, the maturity of liabilities, and the liquidity of assets to determine the risk level of lending or investing in the business.

- Regulatory Compliance: Many regulatory frameworks require businesses to present classified balance sheets to ensure that financial reporting standards are met. It provides transparency, allowing regulators to evaluate financial health and adherence to accounting principles.

How to Prepare a Classified Balance Sheet

Preparing a classified balance sheet involves gathering financial data and then grouping similar items together. Here are the steps typically involved in creating one:

- Organize the Assets:

- List all the assets of the business in order of liquidity, starting with the most liquid (cash and cash equivalents) to less liquid (property, plant, and equipment).

- Organize the Liabilities:

- List all liabilities in order of maturity, starting with short-term liabilities (due within one year) and then long-term liabilities (due after more than one year).

- Calculate Equity:

- The equity section is calculated by subtracting total liabilities from total assets.

- Prepare the Balance Sheet Report:

- Present the classified balance sheet in a format where each section—assets, liabilities, and equity—is clearly separated and aligned. The total assets should always equal the total liabilities plus equity.

Examples of Classified Balance Sheet Presentation

A classified balance sheet typically looks like this:

Conclusion

The classified balance sheet is an essential tool for both financial reporting and decision-making. By classifying assets, liabilities, and equity, it offers clarity and precision in understanding a company’s financial position. It not only helps in evaluating liquidity, solvency, and financial health but also aids in long-term financial planning and risk assessment. For businesses, investors, and financial analysts alike, a well-prepared classified balance sheet serves as a vital instrument in achieving financial clarity and sustainability.